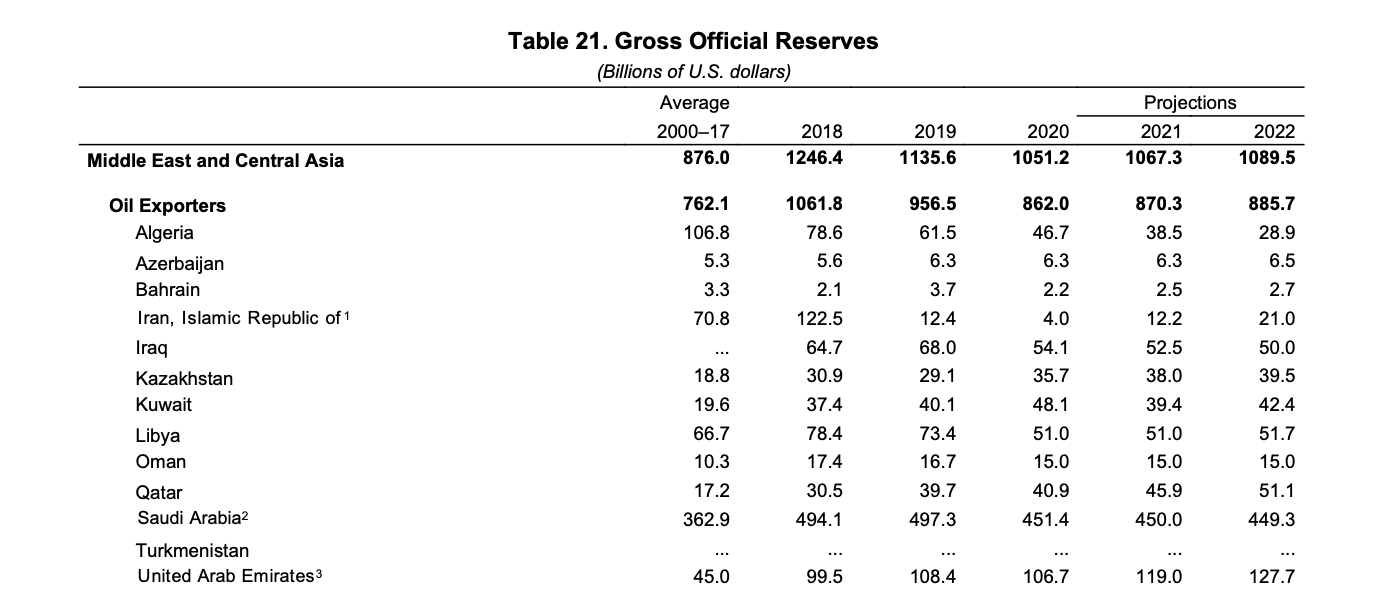

Iran burned through nearly all of its cash reserves in the final years of the Trump administration as harsh economic sanctions crippled the country’s economy and brought the hardline regime to the brink of financial collapse, according to findings published by the International Monetary Fund.

The Islamic Republic had $122.5 billion on hand in 2018 and just $4 billion by 2020, when the former administration’s "maximum pressure" campaign on Tehran was at its height, according to the IMF’s 2021 Middle East and Central Asia report, which tracks the region’s economies. Iran burned through $118.5 billion in two years, nearly depleting its cash reserves. The country’s coffers are forecast to grow by several billions in the coming years as the Biden administration moves to unwind sanctions as part of an effort to reenter the 2015 nuclear deal.

The IMF’s findings are the clearest evidence to date that the years-long U.S. sanctions campaign was successful in emptying the regime’s pocketbook at a time when Iran was spending great sums on its foreign terrorism enterprise and nuclear enrichment program. Sanctions gutted Iran’s oil trade, a key source of revenue for the regime, and forced it to tap heavily into reserve funds. While liberal critics of this approach claim that sanctions only hurt the Iranian people, the IMF’s findings show the hardline regime was under more economic stress than previously known. It is also likely that Iran would not have been able to weather another four years of the Trump administration’s sanctions. Former secretary of state Mike Pompeo said 96 percent of Iran's foreign exchange reserves were "wiped out" as a "direct result of our maximum pressure campaign."

Any sanctions relief granted by the Biden administration in its new diplomatic talks with Iran will provide the regime with a much-needed lifeline for survival. The country’s dire economic situation has generated several waves of democratic protests that threaten to depose the ruling clerical mullahs. Iran’s interest in restarting discussions with the United States early in the Biden administration’s first term signals the regime is desperate for sanctions relief and recognizes that its grip on power is under threat.

The IMF projects that Iran’s reserves will grow to $12.2 billion in 2021 and $21 billion by 2022. That number could be higher if the Biden administration unwinds sanctions and clears the way for international businesses to reinvest in the Iranian economy. The Obama administration adopted a similar approach in 2015, when it first negotiated the deal and removed many of the toughest sanctions in place.

Still, economic forecasts for Iran look dire.

U.S. sanctions on Iran’s illicit oil trade are likely to continue, according to the IMF report. This has forced Iran to peddle its oil at a heavy discount and under the radar. Iran is still producing several million barrels of oil a day, though much of that is being surreptitiously sent to war-torn Syria, where Iranian forces continue to back embattled strongman Bashar al-Assad. These shipments, however, have come under increasing strain. Israeli forces have begun to target Iranian ships ferrying oil to Syria, including at least a dozen ships since late 2019.

Inflation also continues to soar in Iran, according to the IMF report, another sign that sanctions are biting into the country’s economy.

"For the last several years proponents of a renewed deal with Iran have been arguing that max pressure wasn’t working. These numbers tell a different story," said Jonathan Schanzer, senior vice president for research at the Foundation for Defense of Democracies think tank and former terrorist finance analyst at the Treasury Department. "If these numbers still represent the current reality, the United States has far more leverage over the regime than previously believed. The administration should use that leverage at the negotiating table."

Abdolnaser Hemmati, the chair of Iran's Central Bank, which also has been subjected to U.S. sanctions, called the IMF's findings "egregious" on Tuesday. Hemmati said the IMF did not consult with Iran on its report and claimed it contained "incomplete information," though he did not provide proof to support this claim.

Meanwhile, Iran announced on Tuesday that it has begun enriching uranium to the 60-percent level, the highest ever performed by the country and a level that is dangerously close to weapons-grade fuel. The announcement comes after a cyber-attack on the country’s Natanz nuclear facility, which is believed to have been carried out by Israel.

Iran leaders also said this week that nuclear enrichment work will not cease until the United States lifts all of its sanctions as a precondition. This includes all sanctions that were applied by the Trump administration, according to Iranian foreign minister Javad Zarif.

Iranian officials are additionally calling on South Korea to release around $7 billion tied up in the country as a result of sanctions. Iran seized a South Korean tanker and its crew earlier this year and used them as ransom to force a payment of $1 billion, which the Biden administration reportedly signed-off on.