Throughout the 1920s and '30s, many economists were preoccupied by a topic given poignancy by the dramatic economic ups and downs experienced by most Western countries following the carnage of the First World War.

The origins of what came to be called business cycle theory can be traced back to the late 1810s as some scholars of the time tried to comprehend why there appeared to be periodic crises in the industrial capitalism starting to emerge throughout Europe. In the post-World War I era, however, the desire to understand the causes of these recessions—and, occasionally, depressions—acquired urgency because of the political instability associated with severe economic downturns and the impetus they gave to radical movements on the left and right.

In general terms, the business cycle is understood as beginning with a period of economic expansion. Eventually this reaches a peak that marks the start of a downturn. This is followed by a period of economic contraction that ultimately hits a trough, after which the economy starts to recover and enters a new expansion phase.

In the 1930s, many economists were driven to understand what drives this process because they wanted to use state intervention to moderate the "ups" and alleviate the "downs," to the point whereby these fluctuations could be significantly stabilized. John Maynard Keynes and his disciples were emblematic of this position. Others, like F.A. Hayek, however, concluded that such interventions could do little to alleviate economic contractions and might even slow down and distort the recovery phase.

Since World War II, economists have developed theories to try and explain the business cycle's ups and downs. They have also identified indicators to give us a sense of what phase of the business cycle we may be in.

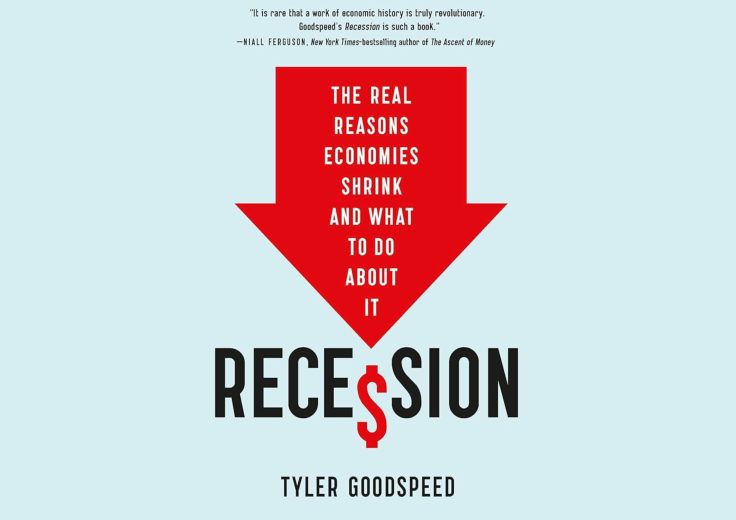

But what if it is the case that there is nothing cyclical at all about the economy's fluctuations? This is a key question raised by the economist Tyler Goodspeed in his new book, Recession: The Real Reasons Economies Shrink and What to Do About It. A former chair of the Council of Economic Advisers and presently chief economist at ExxonMobil, Goodspeed is an accomplished scholar who has published books on topics ranging from the Keynesian revolution in economics to 18th-century Scottish banking.

In all these works, Goodspeed integrates attention to economic theory and history with analysis of existing datasets. But he is also adept at deploying language and concepts drawn from other disciplines to add precision to his arguments.

This way of proceeding is replicated in Recession. The book's core thesis is that recessions are usually sparked by unforeseen external shocks to the economy in the form of events such as natural disasters, the outbreak of war, plagues, or pandemics. Goodspeed also regards many such jolts as emanating from mistaken government interventions that end up inducing and prolonging periods of economic contraction.

To make his case, Goodspeed looks primarily at major recessions that have occurred in Britain and America going back to the 18th century. The available data, Goodspeed argues, makes it difficult to discern any business cycle-like patterns to the process of economic growth and contraction. He also maintains that "the forecasting record of the business cycle indicators" initially developed by the National Bureau of Economic Research in the late 1950s "is unimpressive." This and other critical datapoints illustrate, according to Goodspeed, that the causes of recessions are better described as idiosyncratic.

In making his argument, however, Goodspeed stresses the impact of another factor. He contends that much of the sway on our imagination of arguments that economic growth and recessions are essentially driven from "inside" the economy through factors such as overinvestment in particular economic sectors is derived from our propensity to think in terms of narratives of fall and redemption, such as we find expressed in novels and biblical texts. This inclines us, Goodspeed argues, to understand recessions as purifying events that wipe the economy clean of our past sins and transgressions.

While that outlook is appropriate in other contexts, Goodspeed contends that it tends to blind us to what is really happening in the economy. We become, he says, like a hypochondriac who is "forever identifying illnesses in an otherwise generally healthy economic host." Alas, such a mindset can also lead us to make serious policy errors. "While our pattern-seeking nature may often lead us to protect ourselves against harm," Goodspeed avows, "it can … also lead us to mistakenly avoid otherwise innocuous behavior, or, worse, engage in ostensibly remedial behavior that is in fact counter-productive." From this standpoint, government interventions to address imminent or existing recessions can effectively amount to another type of external shock.

The consequences of Goodspeed's thesis extend beyond the economy. If recessions are unrelated to some defect in the preceding economic expansion, we may have to accustom ourselves to accepting, in his words, "a depressing degree of powerlessness" when an economic contraction is underway. That is a difficult proposition to sell to politicians and voters, most of whom will declare we must do something to counter the decline in investment and the growth in unemployment that characterizes recessions.

This, however, is even more reason, Goodspeed insists, to underscore that "economic expansions endure unless interrupted by shocks that are external to the growth process itself." Certainly, there may be a need for "palliative and pastoral care," suggests Goodspeed, to ward off political problems when shocks occur. Yet we should not make the mistake, he states, of resorting to "prophylactic surgery and puritan asceticism" in response to recessions.

Goodspeed's argument is certainly iconoclastic. After all, it challenges anyone committed to the idea that the state can master economic downturns. But it also represents a substantial rebuff to any school of thought that sees recessions as primarily caused by factors internal to the economy.

Reflecting on this second point, however, I started to wonder whether Goodspeed's theory might contain an element of straw-manning. I can think of few business cycle theorists who offer exclusively internal rationales for recessions. Economists studying this topic generally offer hybrid explanations that present recessions as emerging from a mixture of internal and external causes. Goodspeed's argument, it seems to me, does not grapple with this point.

This criticism aside, Goodspeed provides us with good reasons for greater skepticism about the habit of thinking about the economy in terms of "cycles." Some will find this conclusion pessimistic insofar as it indicates significant limits to the capacity of governments to manage economies. On the positive side, however, Goodspeed gives us some hope that the more we focus on getting essentials like property rights and the rule of law right, and the less we panic in response to sudden events, the greater the likelihood of sustained economic expansions. And that is no small hope to have in our own time.

Recession: The Real Reasons Economies Shrink and What to Do About It

by Tyler Goodspeed

Basic Venture, 310 pp., $30

Samuel Gregg is president of the American Institute for Economic Research. His most recent book is The Next American Economy: Nation, State, and Markets in an Uncertain World (2022), and he can be followed on X @drsamuelgregg.