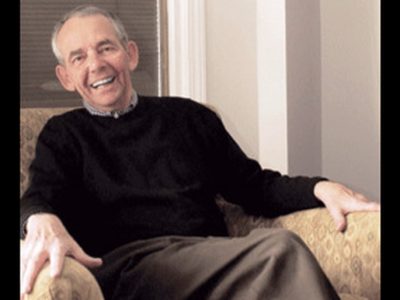

Peter Wallison noticed something odd on the Amazon.com page for his new book.

Immediately after its publication last month, a throng of online commenters gave it overwhelmingly negative reviews. They called his account of the 2008 financial crisis "not truthful," "biased," and "not accurate," though none of the reviews indicated that they had actually read his book. More than 60 commenters rated it one star.

The publisher, Encounter Books, eventually figured out what was happening—a blogger, someone named Tim Howard, had encouraged readers of his website to assail the book on Amazon.

Wallison wryly noted in an op-ed for the Daily Caller that his "book got trolled by the Left" in the latest "expression of the intolerance and bigotry that has begun to infect much of the Left’s attitude toward any dissent."

"Hidden In Plain Sight, for anyone who might care to actually read it, makes a data-based case that the financial crisis was caused by the government’s housing policy," Wallison wrote. "Yes, this contradicts the Left’s desire to show the government as omni-competent and omniscient, but we have to understand why the 2008 financial catastrophe happened in order to avoid pursuing the same policies in the future. This issue needs a robust debate, with facts."

Wallison, a fellow at the American Enterprise Institute and a former general counsel for the Treasury department during the Ronald Reagan administration, sets out to challenge a narrative that congealed almost immediately after the 2008 calamity. Rather than insufficient federal regulation of financial markets on Wall Street, the real culprit was the government’s own policies.

In 1992, the "Federal Housing Enterprises Financial Safety and Soundness Act" was enacted. The new law required Fannie Mae and Freddie Mac—mortgage giants known as "government-sponsored enterprises" (GSEs)—to guarantee more home loans for low-income borrowers. But the loan stipulations proved to be neither safe nor sound. As the GSEs’ regulator, the Department of Housing and Urban Development (HUD), gradually raised the low-income mortgage goal from 40 percent of all loans in 1996 to 56 percent by 2008, Fannie and Freddie were forced to drastically lower their standards.

The GSEs began backing mortgages with down payments of less than 5 percent for borrowers with weak credit histories. Private lenders such as Countrywide Financial Corporation saw the market opportunity for selling risky "subprime" loans to the GSEs and profited handsomely. The contagion of loose lending standards then spread to the wider market as Countrywide and other private firms began to package their own risky loans in mortgage-backed securities. Yet the government remained the principal guarantor. By 2008, federal agencies were exposed to three-fourths of the subprime loans in the market, with Fannie and Freddie accounting for most of them.

Market watchers were shocked when these mortgages defaulted in large numbers in 2008 and depressed home prices by 30 to 40 percent. Perhaps they would not have been if Fannie and Freddie had publicly disclosed that 22 million of the mortgages the GSEs underwrote were, in fact, subprime loans—not prime ones. The Securities and Exchange Commission (SEC) sued former Fannie and Freddie executives in 2011 for allegedly misrepresenting the nature of their loans; the suit is still pending.

Barack Obama showed no inclination after his 2008 election to investigate the government’s disastrous housing policies. Instead, he signed the "Dodd-Frank Wall Street Reform and Consumer Protection Act" into law in July 2010—which passed the House without a single Republican vote and the Senate with just three GOP votes—and blamed the crisis on the financial industry. "Because of this law, the American people will never again be asked to foot the bill for Wall Street’s mistakes," Obama declared at the signing ceremony for the act. "There will be no more tax-funded bailouts—period."

Whether Dodd-Frank will actually prevent another financial catastrophe or not—and the evidence that it would is dubious—the law essentially exonerated the GSEs and the affordable-housing goals despite their central role in the crisis. Congress didn’t even bother to wait for the results from its own Financial Crisis Inquiry Commission (FCIC), which issued its report six months after the law passed.

Wallison was the lone dissenter on the FCIC to place the blame squarely on government-housing policies for the crisis. And he is still waging a lonely fight. Journalists, politicians, and activists were all captured by the Left’s narrative of insatiable greed on Wall Street and inadequate regulation, and they never looked back after Dodd-Frank.

The most revealing aspect of Wallison’s analysis is his discussion of the "government-mortgage complex." This is the web of realtors, homebuilders, mortgage lenders, community activists, sympathetic lawmakers, and corroborative think tanks that provided the real impetus for the affordable-housing goals.

Prominent Democrats including James Johnson (a well-known political operative and former Fannie chairman) and Andrew Cuomo (HUD secretary during the Clinton administration and now governor of New York) advocated for the loans to low-income borrowers as a means of maintaining congressional support for the GSEs and preserving their plans for expansion. Democratic lawmakers such as Reps. Nancy Pelosi (D., Calif.) and Barney Frank (D., Mass.) were only too happy to champion the goals as they cashed in hundreds of thousands of dollars in campaign checks from the real estate, home building, and bank lending industries. And think tanks such as the Urban Institute pushed Fannie and Freddie to serve even more low-income homebuyers as it donated to Democrats and collected government contracts worth millions. What the Left called an altruistic concern for low-income individuals really became one of self-interest.

Wallison believes the same lobby is currently creating the conditions for another future crisis. Mel Watt, director of the Federal Housing Finance Agency (FHFA)—now the regulator of the GSEs—announced in December that Fannie and Freddie would again back loans with down payments as low as 3 percent, but without abandoning "safe and sound lending practices" (language borrowed from the 1992 goals). It should come as no surprise that Watt garnered thousands in campaign contributions from the real estate and lending industries when he was a Democratic congressman for North Carolina.

Obama also extoled a cut last month to annual premiums on mortgages insured by the Federal Housing Administration (FHA)—loans that are typically even riskier than those guaranteed by the GSEs and have required sizable bailouts before. Lastly, six federal agencies in October issued the final definition for a "qualified residential mortgage"—intended to be the new gold standard for a prime mortgage loan—as required under Dodd-Frank. However, they decided upon a definition so weak that it lacked any down payment or credit requirements.

"How we view the past affects what we do in the future," Wallison writes. "If we have failed to correctly assess what caused the financial crisis, we will stumble blindly into another one in the future. And that, indeed, seems to be where we are headed."

For some readers, Wallison will seem at times to venture into an uncomfortable level of technical detail in his attempt to present a comprehensive account of the financial crisis—but no one can fault him for a lack of data to back his assertions. His book is meticulously researched and forwards an alternative narrative of the crisis that the current administration finds politically inconvenient. Above all, Wallison’s book makes the case that acting upon the lessons of the past first requires understanding what those lessons really are.